300x85.png)

Hong Kong

Hong Kong Singapore

Singapore China

China Dubai

Dubai Thailand

Thailand United Kingdom

United Kingdom Mexico

Mexico

Both travel insurance and short-term international health insurance protect your health while abroad as a visitor. Travel insurance protects against a range of travel-related risks, and short-term international health insurance offers coverage for health-related risks.

Discover the world’s top

health insurers.

Compare quotes with

a click of the button.

In addition to travel insurance and short-term international health insurance, you may also want to consider expat health insurance and international health insurance. They are designed for different needs, and there are significant differences among them.

In this article, we explain these types of insurance in detail and how you should choose among them. We’ll also cover medevac insurance, which covers the cost of medical evacuation or repatriation should that become medically necessary.

Travel Insurance

Travel insurance provides coverage for a variety of risks that travelers may encounter on their trip, and one of its crucial functions is to protect the health of visitors against injuries, medical emergencies, and infectious diseases.

Travel insurance typically includes coverage for medical expenses incurred due to unexpected illnesses or injuries during the trip, including:

- Hospitalization

- Doctor visits

- Prescription medications

- Emergency medical evacuation if necessary

Moreover, travel insurance often provides a 24/7 helpline for medical advice, coordination of medical services, and assistance in locating suitable medical facilities. These services can be invaluable when visitors may face language barriers or difficulty navigating the local healthcare system.

However, travel insurance has its limitations. For starters, most travel insurance policies do not cover medical expenses related to pre-existing conditions. Individuals with pre-existing conditions should thus consider other insurance options which may provide coverage for these conditions.

Additionally, the coverage period of travel insurance is limited, and while the health-related protection it offers may vary depending on the specific policy, the emphasis is generally on addressing and managing emergencies rather than providing comprehensive or long-term care.

Individuals planning to stay abroad for an extended period, such as expats or digital nomads, may thus need to explore alternative insurance options, like expat health insurance or international health insurance.

Short-term International Health Insurance

Short-term international health insurance offers comprehensive medical coverage for individuals who are temporarily abroad for up to 12 months. This insurance provides coverage throughout their time spent overseas.

Short-term international health insurance covers the cost of medical treatment while abroad, including:

- Emergency medical care

- Hospital stays

- Specialist consultations

- Emergency medical evacuation

- Unexpected health issues such as accidents and illnesses

Visitors can choose a policy that suits their specific travel period, ranging from 1 to 12 months. You can thus have adequate health coverage for your overseas stay without committing to a long-term insurance plan. Typically, you can extend your coverage if needed.

However, like all insurance plans, short-term international health insurance has limitations. For example, pre-existing conditions are typically excluded from coverage. Some insurers may offer optional riders to cover pre-existing conditions, but additional costs or restrictions often follow.

Routine or pre-planned treatments in the individual’s home country are also usually not covered. Additionally, certain high-risk activities, such as extreme sports or hazardous occupations, may be excluded from coverage.

When it comes to maternity coverage, short-term international health insurance may provide limited coverage or exclude it altogether. Pregnancy is often considered a pre-existing condition, and insurers may have specific waiting periods before maternity benefits become available.

Although some policies offer limited coverage for complications arising from pregnancy, routine prenatal care and childbirth expenses are rarely covered. Expectant mothers should thus review the policy terms before relying on short-term international health insurance for maternity-related expenses.

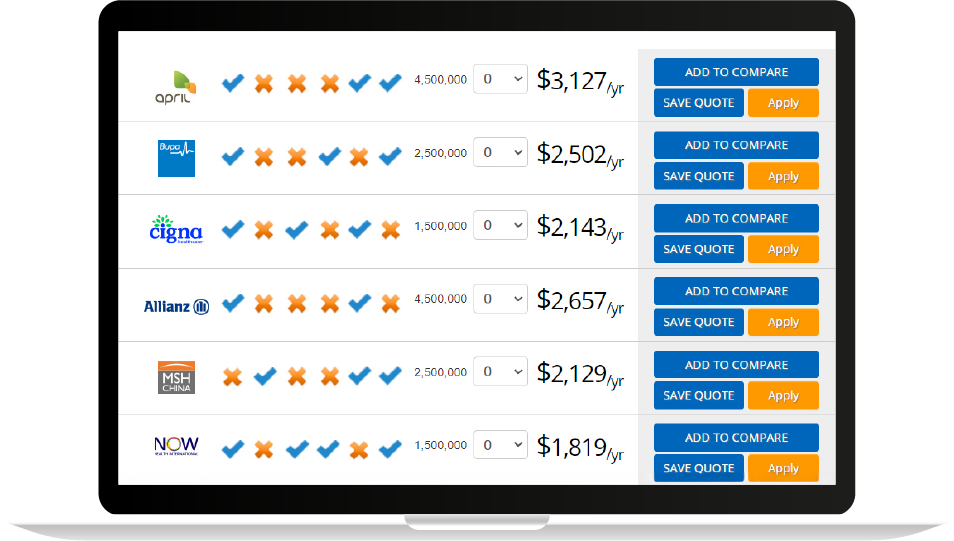

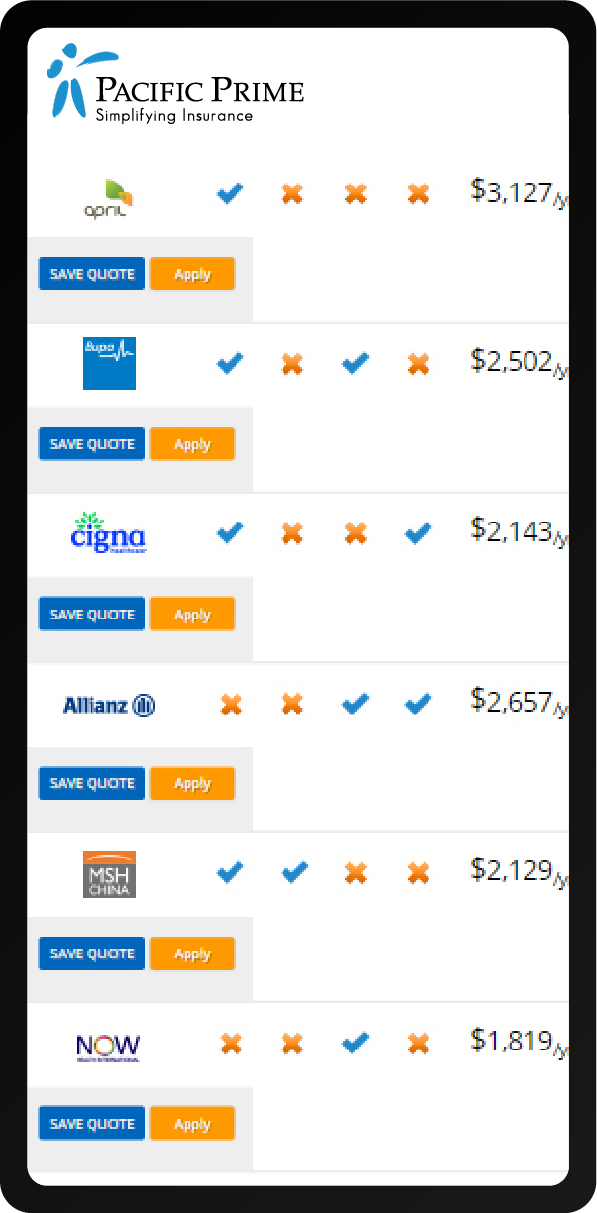

Summary of Your Health Insurance Options as a Visitor

Below is a table comparing the key aspects of travel insurance and short-term international health insurance. Expat health insurance and international health insurance are also included in the comparison because many people end up securing these coverages after learning more about them.

| Travel Insurance | Short-Term International Health Insurance | Expat Health Insurance | International Health Insurance | |

| Coverage Duration | Duration of the trip | 1 to 12 months | Usually long-term (1+ years) | Varies (often long-term) |

| Purpose | To protect against trip-related risks | To provide health coverage for temporary stays abroad | To provide health coverage for long-term living abroad | To provide health coverage with international mobility |

| Medical Coverage | Limited | Comprehensive | Comprehensive | Comprehensive |

| Trip-related Coverage | Trip cancellation, baggage damage or loss, travel delays, etc. | Limited or none | Limited or none | Limited or included depending on the policy |

| Pre-existing Conditions | Typically not covered | Typically not covered by default | Coverage varies | Coverage varies |

| Inpatient Care | Limited coverage or none | Covered | Covered | Covered |

| Outpatient Care | Limited coverage or none | Covered | Covered | Covered |

| Preventive Services | Limited coverage or none | Coverage varies | Coverage varies | Coverage varies |

| Dental Coverage | Limited coverage or none | Coverage varies | Coverage varies | Coverage varies |

| Vision Coverage | Limited coverage or none | Coverage varies | Coverage varies | Coverage varies |

| Coverage Territory | Varies depending on the policy | Worldwide coverage possibly with excluded region(s) | Coverage in specified country(ies) | Worldwide coverage possibly with excluded region(s) |

| Renewability | Not applicable | Typically renewable for up to a year | Renewable | Renewable |

| Suitable for | Tourists, occasional travelers | Longer overseas trips, students, short-term work assignments | Expats, long-term residents, employees | International travelers, digital nomads, individuals with global mobility |

This table provides only a general comparison. Specific details may vary depending on the insurer and policy terms.

Medevac Insurance

Medical evacuation insurance, also known as medevac insurance, covers the transportation of an injured or ill individual to a medical facility capable of providing adequate treatment. It ensures that individuals receive necessary medical care in a medical emergency while traveling.

Medevac insurance usually covers transportation by air or ground ambulance, and sometimes even by sea, depending on the seriousness of the situation and the individual’s location.

Medevac plans commonly include 24/7 emergency travel assistance services, and further cover the cost of:

- Medical repatriation

- Return of accompanying dependent children

- Return of mortal remains should a covered individual, unfortunately, pass away while traveling

Medevac coverage is often included in travel insurance and international health insurance plans. However, standalone medevac insurance plans often provide more elaborate medical evacuation services, greater flexibility and customization options, and higher coverage limits.

Standalone policies also tend to offer better coverage for pre-existing medical conditions. With a standalone policy, there is no risk of other travel insurance benefits being affected by the use of medical evacuation services because it is a separate policy purely focused on medical evacuation.

For a detailed explanation of medevac insurance, please click here.

How You Should Choose an Insurance Policy

Choosing the right insurance always begins with a good understanding of your needs. We recommend that you follow the steps below to make sure the plan you secure is exactly what you need:

- Carefully assess your insurance needs, and make sure the right risks are covered.

- Shop around, and seek out plans with sufficient coverage limits.

- Choose an insurer with a strong reputation for efficient service, good 24/7 multilingual support, and fairness.

- Make sure the insurer has a sizable service provider network, and your preferred service providers are in the network.

- Pick a plan with premiums you can afford, bearing in mind that plan premiums often depend on the deductibles and copayments you select.

- Understand the exclusions and limitations of the plan, particularly with regard to coverage for pre-existing conditions and waiting periods.

- Check whether the insurer will pay service providers directly because it can create tremendous financial hardship for the client otherwise.

- Read the policy terms carefully before signing on the dotted line, and take note of the various requirements and restrictions; it is also important to understand the claims process and the documentation you need to produce when making a claim.

Consult with a Travel Insurance Broker or Specialist

An insurance brokerage with international experience can help you navigate through the available options and provide personalized recommendations with your needs and budget in mind. What’s more, the value for money of their recommendations is hard to beat because they are familiar with the market.

Frequently Asked Questions

What are the main health insurance options available to visitors?

Travel insurance and short-term international health insurance are the two main types of health insurance plans for travelers. However, depending on the individual’s circumstances, expat health insurance or international health insurance could serve their needs even better.

What is medevac insurance, and how can I secure this insurance?

Medevac insurance ensures that individuals receive prompt and adequate medical care by transporting them to suitable facilities if medically necessary. Travel insurance and international health insurance plans often include this coverage. Standalone medevac insurance plans are also available.

What are the main things to pay attention to when choosing among health insurance plans?

The main criteria include covered risks, coverage limits, exclusions and limitations, insurer reputation, support from the insurer, premium levels, deductibles, copayments, size of the service provider network, whether the insurer will pay service providers directly, and the policy terms.

Conclusion

In this article, we’ve focused on helping readers choose the right health insurance for their overseas trip or stay. We’ve also compared and contrasted travel insurance and short-term international health insurance with some other similar types of insurance.

Insurers are forever trying to outshine each other with new products with higher limits, improved flexibility and adaptability, wider coverage, and more features, and it is some real work to keep up with their latest offerings. That’s why so many people work with us when securing health insurance.

Whether it’s travel insurance, short-term international health insurance, expat, or international health insurance, We have the expertise and experience to tailor a solution that fulfills your requirements within your budget.

What’s more, you will benefit from our advice and support at no extra cost, and you can be sure our recommendations represent the best value for money. So contact us for a quote or a FREE plan comparison today!

Are you going to Malaysia or Europe soon? If so, Health Insurance in Malaysia for Foreigners: A Comprehensive Guide and Health Insurance in Europe: A Guide for Expats will exactly serve your needs, just like the plans we recommend will fit your requirements and budget!

Since joining Pacific Prime, Martin has become even more aware of the gap between the true value of insurance products and most people’s appreciation of it, and developed a passion for demystifying and simplifying matters, so that more people get the protection they need at a cost they can easily afford.

In his free time, Martin attends concerts of various genres, and plays the violin with piano accompaniment he pre-recorded himself or played live by his niece.

- Bali Visa on Arrival: Essential Guide for Travelers – October 17, 2025

- Cost of Living in Costa Rica: Expat Guide – October 15, 2025

- Top 11 Insurance Companies in Curaçao for Expats – October 8, 2025