300x85.png)

Hong Kong

Hong Kong Singapore

Singapore China

China Dubai

Dubai Thailand

Thailand United Kingdom

United Kingdom Mexico

Mexico

It is common for pre-existing conditions to be excluded from coverage in Malaysian health insurance for expats. Cigna, Allianz, and Bupa may provide coverage, depending on your medical history. To find coverage, expats should consult an insurance broker who can help them negotiate the best deal.

Discover the world’s top

health insurers.

Compare quotes with

a click of the button.

Are you an expat or foreigner in Malaysia trying to find pre-existing conditions coverage? Are you not sure which conditions are usually excluded and which providers can cover them? This Pacific Prime blog post is designed to explain all of that for you!

Not only will we define pre-existing conditions and which types of health concerns are considered pre-existing but also we will also explain common questions such as how waiting periods work, which providers in Malaysia include pre-existing conditions coverage, and much more!

After you’ve finished this article, you’ll want to check out the various health insurance options in Malaysia for expats and learn how Malaysia’s healthcare system works.

What Malaysia Insurance Means by Pre-Existing Conditions

A pre-existing condition in international health insurance refers to any health issue an expat had before their policy began, whether diagnosed, treated, or showing symptoms. Common examples include asthma, diabetes, high blood pressure, or previous surgeries.

For expats in Malaysia, this matters because local insurance plans usually exclude coverage for pre-existing conditions altogether, while international insurers may offer more flexibility. Some global providers impose a waiting period, while others may charge a higher premium.

A few comprehensive expat policies allow coverage if your condition is stable and well-managed, though this varies by insurer.

Without proper coverage, expats in Malaysia risk paying high out-of-pocket costs at private hospitals, which are the main choice for foreigners since public healthcare access is limited. Consider the following tips to avoid this financial trap.

Tips for Getting Pre-Existing Conditions Coverage:

- Understand how pre-existing conditions are defined and treated when choosing insurance in Malaysia.

- Review policy terms carefully so you know what’s excluded, what’s covered, and under what conditions, helping you avoid unexpected gaps in care.

- Consult an insurance broker to find plans from international health insurance providers who offer pre-existing conditions coverage.

Does Malaysia Insurance Cover Pre-Existing Conditions?

Most Malaysian health insurance plans do not cover pre-existing conditions, meaning any illness or treatment you had before buying the policy is excluded. For expats, this can be tricky because local insurers often deny coverage, while international providers may offer limited options.

Such limitations can include waiting periods, higher premiums, or partial benefits depending on your health history. This makes reviewing policy terms essential before choosing a plan.

How Insurers Decide Pre-Existing Conditions Coverage

Expats who are applying for international health insurance in Malaysia go through a medical underwriting process to determine the eligibility of their pre-existing conditions.

This involves the following steps:

- Filling out detailed health questionnaires

- Sometimes providing medical records

- Sometimes having a check-up

Insurers use this information to assess risk and decide how to handle any pre-existing conditions. The outcome can vary, ending in the condition being excluded from coverage, accepted with restrictions, or covered after a waiting period.

For expats, this means your past medical history directly influences not only whether you’re covered but also the cost and scope of your policy. It is essential to be completely honest about this history and to fully disclose all health conditions.

Premium Loading and Coverage Denial

If an insurer determines a pre-existing condition poses higher risk, they may apply premium loading, which means charging a higher monthly or annual premium to offset the likelihood of future claims. In more serious cases, the insurer may issue a coverage denial for that condition.

This means all related treatments are permanently excluded. For expats in Malaysia, this can be a significant challenge, as it may leave you paying out of pocket for essential care if your condition isn’t accepted under the policy.

What Happens if Pre-Existing Conditions Aren’t Declared

If pre-existing conditions aren’t declared during the underwriting process, insurers can void your policy, deny claims, or cancel coverage altogether once the omission is discovered. Even unintentional nondisclosure is treated seriously, as insurers rely on full medical history to calculate risk.

Even if the condition is unrelated to your current claim, failure to disclose is treated as a breach of trust. For expats in Malaysia, this could mean being left without coverage when you need it most and facing expensive medical bills at private hospitals.

Full disclosure is always the safest approach, since some insurers may still offer limited coverage options, waiting periods, or premium loading if conditions are declared honestly.

How Waiting Periods Affect Pre-Existing Conditions

A waiting period (sometimes a moratorium) is the period after the start date of the policy during which treatment for pre-existing conditions is not covered. If you make a claim for that condition before the waiting period ends, the insurer will usually reject it for that condition.

The purpose is to prevent people buying insurance after knowing they need expensive treatment and to balance risk among policyholders.

Waiting periods can be any of the following lengths:

- A few months

- 10–12 months

- 24 months

- 36 month

- 48 months

- Or anything in between!

The length depends on the insurer, policy type, how serious or stable the condition is, plus how much disclosure or underwriting is done.

Some insurers offer moratorium-based plans where you don’t need diagnosis or treatment for a certain continuous time post-policy, and after that period the pre-existing condition may become covered if there have been no symptoms, medication, or treatment required.

Most Common Pre-Existing Conditions that Aren’t Covered

Diabetes, asthma, high blood pressure, cardiovascular conditions, cancer, depression, chronic joint pain, and kidney disease are among the most common pre-existing conditions that aren’t covered by insurers for expats in Malaysia. See our more detailed list below for more.

- Diabetes

- Asthma

- Hypertension (high blood pressure)

- Heart disease/cardiovascular conditions

- Cancer (active, recent treatment)

- Kidney disease (e.g. chronic or recurring)

- Mental health disorders (e.g. depression, bipolar disorder, schizophrenia)

- Thyroid disorders (hypothyroidism, hyperthyroidism)

- Arthritis and joint disorders (rheumatoid arthritis, chronic joint pain)

- Gastrointestinal disorders (e.g. GERD, ulcers)

- Skin conditions/allergies (severe or chronic eczema, food allergies)

- Neurological conditions (e.g. epilepsy, frequent migraines)

- Autoimmune conditions (e.g. lupus, multiple sclerosis)

- Chronic respiratory diseases beyond mild/acute (for example, COPD)

Malaysia Medical Coverage for Pre-Existing Conditions

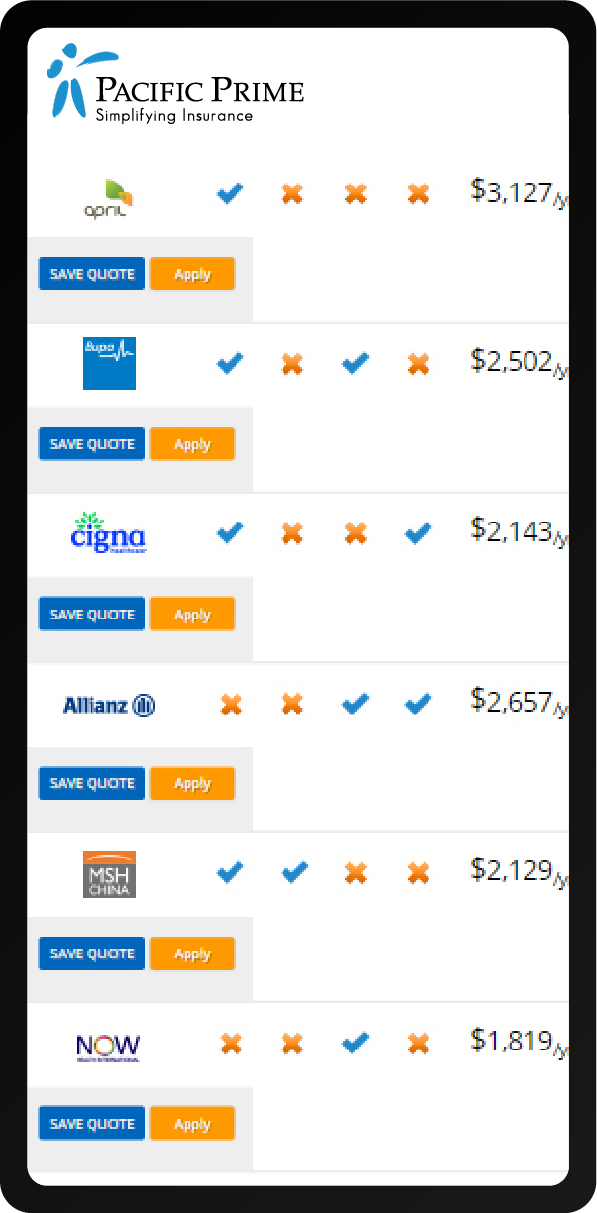

Cigna Global, Bupa Global, Allianz Care, IMG, VUMI, AXA, and APRIL International are international health insurance providers that do offer coverage for expats with pre-existing conditions living in Malaysia.

While these providers have been known to provide coverage before, each person’s medical history is unique, and the provider will consider the severity, stability, and risk of your unique condition in the medical underwriting process before confirming or denying coverage.

Cigna Global – Coverage for Pre-Existing Conditions

Cigna Global can cover pre-existing conditions for expats in Malaysia depending on the medical questionnaire and underwriting. Cigna may add special exclusions or loadings if conditions existed before the policy start date.

Bupa Global – Coverage for Pre-Existing Conditions

Bupa Global uses full medical underwriting to determine the qualifications of a pre-existing condition. They may cover, exclude, or restrict pre-existing conditions depending on the underwriting outcome. Exclusions can be applied per applicant. Moratoriums may be applied.

Allianz Care – Coverage for Pre-Existing Conditions

Allianz Care offers both full medical underwriting (where some pre-existing conditions may be accepted) and moratorium underwriting (commonly a 24-month moratorium, after which previously excluded conditions may become eligible if symptom-free).

IMG – Coverage for Pre-Existing Conditions

IMG Global has a Pre-Existing Conditions Waiver that may allow for coverage of pre-existing conditions if approved at the time of application. Some of IMG’s products may offer limited pre-existing coverage or have specific short waiting periods.

Many of their contracts, however, exclude pre-existing conditions unless specifically declared and accepted.

VUMI – Coverage for Pre-Existing Conditions

VUMI may offer expats in Malaysia coverage for their pre-existing conditions if approved in the underwriting process and the waiting period has passed. For example, their Travel VIP plan covers standard pre-existing conditions after six months if they have been stable without presenting symptoms.

AXA – Coverage for Pre-Existing Conditions

AXA may also offer coverage for pre-existing conditions in Malaysia if approved in the underwriting process. Depending on your contract, you may cover pre-existing conditions according to your medical underwriting, your continued medical exclusions from a previous insurer, or after the moratorium.

APRIL International – Coverage for Pre-Existing Conditions

APRIL International offers an add-on rider for pre-existing conditions coverage with some of their health insurance plans. You’ll want to compare their plans and read all the fine print to determine if the plan you’d like to select comes with this feature or another way to secure your coverage.

Why Insurers Have to Factor in Pre-Existing Conditions

It is essential for insurers to factor in a person’s pre-existing conditions when determining coverage because they have to balance risk, ensure fairness in premiums, and maintain their ability to provide coverage sustainably. If they did not do this, providers could go out of business.

This is why insurers carefully review medical histories during the underwriting process and may apply exclusions, waiting periods, or premium adjustments.

Here’s a deeper look at why insurance companies have to carefully examine how much of a pre-existing condition they can afford to pay for.

Risk Assessment

Pre-existing conditions increase the likelihood that the insured will require medical care. Chronic illnesses, prior surgeries, or ongoing treatments represent predictable costs insurers use to anticipate the overall risk profile of the applicant.

Premium Calculation

Insurance works by pooling risk across many policyholders. If a person has a higher risk of claims due to pre-existing conditions, the insurer may need to charge higher premiums (premium loading) to offset potential losses, ensuring the financial sustainability of the plan.

Coverage Limitations

Insurers may exclude certain pre-existing conditions or impose waiting periods to prevent immediate claims related to known health issues. This avoids situations where someone buys a policy only when they need expensive treatment, which could destabilize the insurance pool.

Financial Stability

By factoring in pre-existing conditions, insurers protect the company’s solvency. Covering high-cost conditions without adjustments could lead to significant financial losses, which would ultimately affect all policyholders.

Regulatory Compliance & Underwriting Standards

Insurers are required to follow sound underwriting practices. Evaluating pre-existing conditions ensures that they comply with actuarial standards and maintain fair risk-based pricing across their insured population.

How Brokers Help Expats Cover Pre-Existing Conditions

Brokers help expats find and negotiate for health insurance plans that offer the best coverage that can be obtained for their pre-existing conditions. They do this by aiding in the research and comparison process and by using their market knowledge and partnerships to find the best deals available.

Insurance brokers are experts on the international health insurance market, and instead of working for insurance companies seeking out new clients, they represent the expats as a third party negotiator between the expat and the insurance provider.

Expats heading to Malaysia with pre-existing conditions should purchase their insurance plans through a broker instead of directly from the insurance company to get the most out of their coverage.

Here are some benefits expats can expect to receive when partnering with an insurance broker:

- You get access to more insurance choices.

- You get experienced insurance experts researching your situation for you.

- You get access to the most cost-effective plans available.

- You get assistance when submitting claims for reimbursement.

- You get expert advice designed to help you find the right plan for you, not to be led to the plan an insurance agent wants you to choose.

There are many more benefits to using a broker, and Pacific Prime is your broker of choice. Let us help you find the right Malaysia travel insurance plan for your budget and needs that include the best coverage possible for your pre-existing conditions. Contact us to learn more!

Frequently Asked Questions

Can Malaysian providers exclude pre-existing conditions?

Most Malaysian health insurance providers exclude pre-existing conditions. This means illnesses or treatments you had before buying the policy usually won’t be covered, making international plans more flexible for expats.

Can expats get full coverage for a pre-existing condition?

Full coverage for pre-existing conditions is rare. Some global insurers may offer it after a waiting period, with higher premiums, or under special terms. Expats often need international health plans to access broader coverage.

How do expats in Malaysia get coverage for pre-existing conditions?

Expats in Malaysia can secure coverage by choosing international health insurers that use medical underwriting, offer moratoriums, or allow premium loading. Working with a broker helps find policies tailored to your health history.

Is a broken leg a pre-existing condition for expats?

A broken leg isn’t usually treated as a pre-existing condition once healed. However, if you have lingering complications, surgeries, or recurring mobility issues, insurers may classify it as pre-existing and limit coverage.

Is back pain a pre-existing condition for expats?

Back pain is usually considered a pre-existing condition if you had symptoms, diagnosis, or treatment before your policy began. Insurers may exclude related care or impose waiting periods.

Is high cholesterol a pre-existing condition for expats?

High cholesterol is typically treated as a pre-existing condition on expat health insurance. Since it raises risks for heart disease, insurers often apply exclusions, waiting periods, or higher premiums for expats with this condition.

Are kidney stones a pre-existing condition for expats?

If you’ve had kidney stones before enrolling in your expat insurance, most insurers classify them as pre-existing. This can lead to exclusions or limited coverage, especially if stones are recurrent or recently treated.

Is GERD a pre-existing condition for Malaysian expats?

GERD is usually seen as a pre-existing condition for Malaysian expats if diagnosed or treated before your policy started. Some insurers may exclude it entirely, while others may offer coverage after a waiting period.

Are varicose veins a pre-existing condition for expats?

Varicose veins are generally considered pre-existing on expat health insurance if you’ve had them prior to coverage. Treatment may be excluded or limited, especially if surgery or ongoing care has already been needed.

Is diabetes a pre-existing condition for expats?

Diabetes is always classified as a pre-existing condition when it comes to international health insurance. Most insurers exclude it or charge expats higher premiums, though some international plans may cover it with restrictions or waiting periods.

Is a bad knee a pre-existing condition for expats?

If an expat has had knee pain, surgery, or recurring issues before their policy started, it counts as a pre-existing condition. Insurers may exclude related treatments or require waiting periods for coverage.

Is a C-section a pre-existing condition for expats?

A past C-section is considered a pre-existing condition, especially if complications or future pregnancies are expected. Some policies may exclude maternity care for expats in Malaysia or related surgeries afterward.

Are gallstones a pre-existing condition for expats?

Gallstones are usually treated as pre-existing if the expat had them before coverage began. Insurers often exclude surgery or treatment unless the condition develops after the policy starts.

Conclusion

This article explained what pre-existing conditions are and how they are treated by insurance companies for expats in Malaysia. If you have a health concern that you believe may be considered a pre-existing condition and be excluded from coverage, consult a broker to find your coverage options.

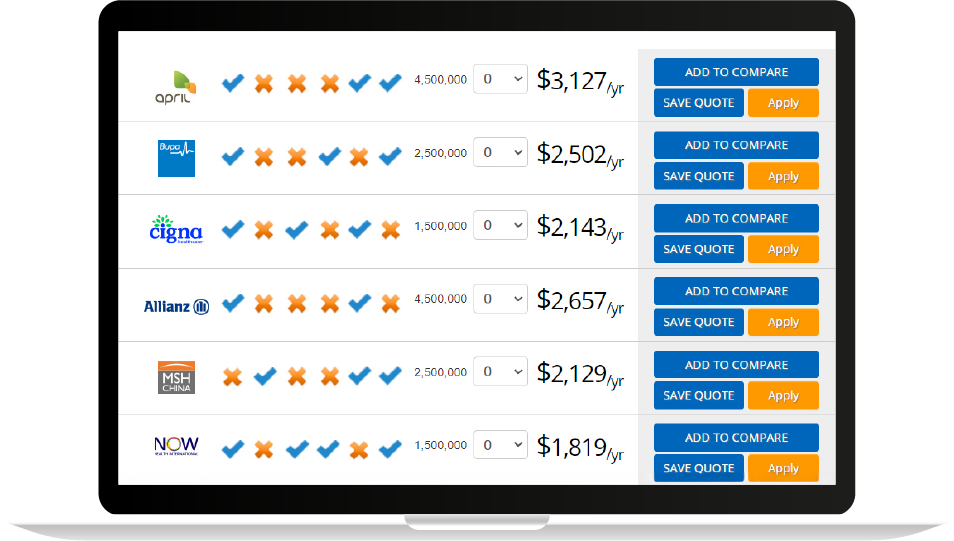

Now that you’re ready to pick a plan, you’ll want to check out our free, online insurance plan comparison tool that has over 50,000 plans saved in our database.

With it, you can compare multiple plans side by side, save your favorite plans for later reference, and get real quote estimates for plans according to your personal information and travel itinerary. Get started today!

If you’d rather speak to a Malaysian insurance expert, contact our team online or over the phone at 1-800-868-1451.

Be sure to read our posts Malaysia Senior & Retirement Visa Health Plans and Short-Term & Visitor Medical Plans for Malaysia as well.

Safe travels!

Serena earned her Bachelor’s Degree in Psychology from the University of British Columbia, Canada. As such, she is an avid advocate of mental health and is fascinated by all things psychology (especially if it’s cognitive psychology!).

Her previous work experience includes teaching toddlers to read, writing for a travel/wellness online magazine, and then a business news blog. These combined experiences give her the skills and insights she needs to explain complex ideas in a succinct way. Being the daughter of an immigrant and a traveler herself, she is passionate about educating expats and digital nomads on travel and international health insurance.

- How to Compare Travel Insurance Plans the Smart Way – October 21, 2025

- Best Hospitals in the UAE: Top Picks in Dubai and Abu Dhabi – October 21, 2025

- How Much is a Doctor Visit in Dubai Without Insurance? – October 21, 2025