300x85.png)

Hong Kong

Hong Kong Singapore

Singapore China

China Dubai

Dubai Thailand

Thailand United Kingdom

United Kingdom Mexico

Mexico

Takaful insurance complies with Islamic law and is based on principles of cooperation and sharing, while conventional health insurance does not. In takaful insurance, the funds are owned by those contributing to the insurance fund and not by the insurance company.

Discover the world’s top

health insurers.

Compare quotes with

a click of the button.

Are you an expat who needs health insurance for Malaysia, and want to know more about takaful insurance? Are you unsure of how it differs from conventional health insurance plans? The insurance experts at Pacific Prime have created this guide to help you understand the differences between the two.

We will share an overview of each type of insurance, key differences between the two, and more. Continue reading to learn more, or click here for a free health insurance quote for Malaysia!

How Takaful Insurance Works in Malaysia

A takaful insurance plan works by allowing individuals to pool their money together to insure against losses or damage. Takaful insurance can offer life insurance, home insurance, and health insurance to individuals or families in Malaysia.

Takaful insurance is most common in countries with large Muslim populations, as it conforms to Islamic religious law. You do not have to be Muslim to purchase takaful insurance, as it is open to anyone from any religious background.

Takaful insurance operates through the following steps:

- Participants agree to pay a certain amount of money to a common pool or mutual fund.

- Participants make regular contributions to the takaful mutual fund.

- The fund is managed and administered by a takaful insurance operator. This operator is responsible for paying the claims made by participants.

- If there is a loss, the takaful operator will pay the claim from the fund.

- At the end of the agreed period of the policy, the surplus funds from the takaful fund are shared among the participants and the operator.

Takaful operators charge a fee for their costs, which will cover services like underwriting, sales, and marketing, in addition to claims management.

Takaful insurance was created to be Sharia-compliant. Sharia, the Islamic religious law, restricts riba (interest), al-maisir (gambling), and al-gharar (uncertainty) principles, which are believed to be associated with the conventional insurance market.

Top Takaful Insurance Companies in Malaysia

Some of the top takaful insurance companies in Malaysia include Zurich Malaysia, Takaful Malaysia, AMAN Takaful, and Etiqa.

How Conventional Health Insurance Works in Malaysia

Conventional health insurance in Malaysia works by policyholders paying monthly or annual premiums to their insurance companies, who then agree to cover medical costs for the policyholder as long as they abide by the provider’s policies.

Conventional private health insurance typically operates by the following steps:

- The policyholder pays a monthly (or annual) premium to an insurance company to maintain their coverage.

- The policyholder receives medical care through an in-network healthcare provider or healthcare facility.

- The policyholder pays toward their deductible for covered services.

- The policyholder will pay coinsurance with the insurance company once the deductible has been met.

- The policyholder reaches their out-of-pocket maximum, and the insurance company then pays 100% of healthcare costs until the end of the policy period.

Some conventional health insurance key terms to understand are the following:

- Premium: The fixed amount you pay to the insurance company every month, or year if you choose to make an annual payment. You pay this to keep your coverage active, and you will be required to pay it regardless of whether you did not use your health insurance plan.

- Deductible: The amount the policyholder pays before the insurance company begins to pay. Insurance companies usually offer a variety of plans that range from low deductible to high deductible. Low-deductible plans are generally more expensive.

- Coinsurance: Coinsurance is the cost-sharing percentage you will pay after you’ve met your deductible. The insurance company will cover the rest of the cost of the medical services. The percentage amount will vary by plan, but policyholders paying a 10–20% coinsurance is common.

- Out-of-pocket maximum: This is the total amount the policyholder will be responsible for paying for covered medical services that year. Once you hit this limit through paying your deductible and coinsurance, your insurance provider will pay 100% of your covered costs for the rest of the year.

- In network: In network means there is a contractual agreement with your health insurance plan and a health care provider or facility regarding a pre-negotiated amount they’ll charge for their medical services. Receiving in-network care means you will usually be paying less for your medical care.

Popular Conventional Health Insurance Companies in Malaysia

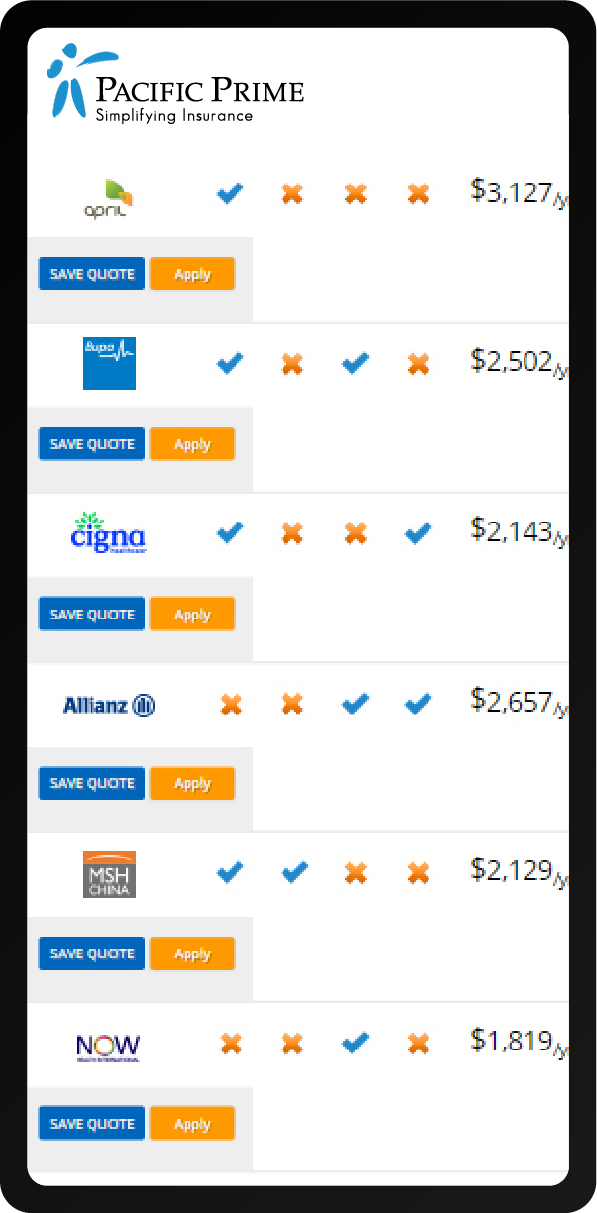

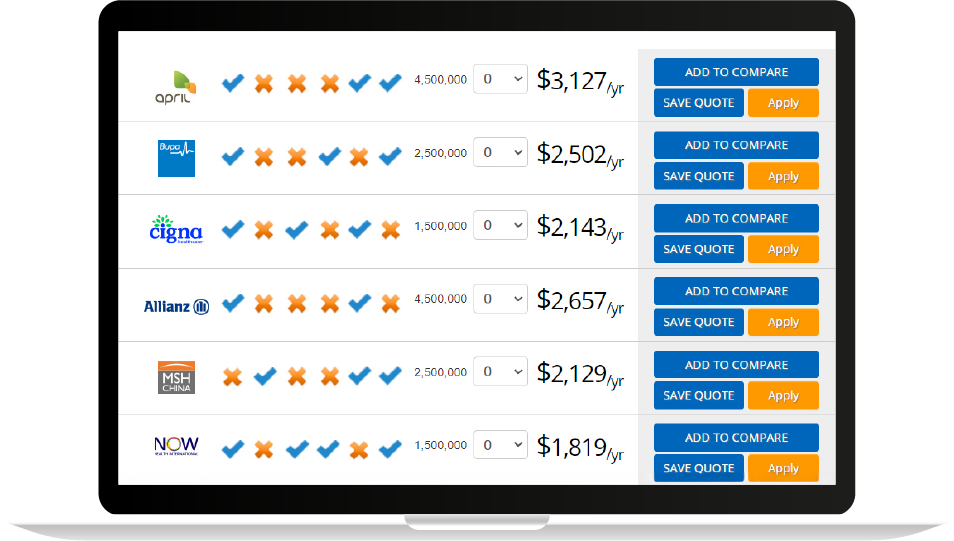

Some of the top conventional health insurance companies in Malaysia are Cigna Global, Bupa Global, Allianz, and AXA. These international health insurance companies offer the added benefit of global coverage to their comprehensive and customizable plans.

Key Differences Between Takaful and Conventional Health Insurance in Malaysia

The key differences between takaful and conventional health insurance in Malaysia are the ownership of the funds, the risk management, Sharia compliance, and the surplus distribution.

While both types of health insurance can help provide medical coverage, they differ in many ways.

1. Ownership of Funds

In takaful health insurance plans, funds are owned by the individuals paying into the takaful fund. In a conventional health insurance plan, funds are owned by the insurance company.

2. Risk Management

In takaful health insurance plans, the risk is shared among the individuals paying into the takaful fund. Any claims that are to be paid must come out of the takaful fund. This can be an issue during times of natural disasters or when many large claims are made at once.

In conventional health insurance, the risk is transferred to the insurance company. The insurance company will solely be responsible for paying for covered costs if the deductible and coinsurance have been met.

3. Sharia Compliance

Takaful is compliant with the Islamic religious law, sharia. Riba (interest), al-maisir (gambling), and al-gharar (uncertainty) principles are restricted by sharia. Takaful insurance is also associated with the concepts of mutual cooperation and shared responsibility.

Conventional health insurance is believed not to abide by sharia law.

4. Surplus Distribution

In a takaful insurance plan, surplus funds will be either distributed back to the individuals who have been paying into the fund or reinvested back into the fund. This can make takaful a profitable investment for some.

Conventional health insurance providers keep all the profits made in a period if the payouts are less than anticipated. Policyholders will still be expected to pay their monthly premiums even if they have not used any medical services or made any claims that month.

Pros and Cons of Takaful and Conventional Health Insurance

Takaful insurance offers the advantage of being an investment strategy for those paying into the fund, though its limited availability in non-Muslim countries may be a disadvantage to some. Conventional health insurance comes with its own strengths and weaknesses.

Takaful Insurance pros:

- Acts as an investment strategy for those paying into the takaful fund

- Complies with sharia law

- Funds are directly owned by those paying into the takaful fund

Takaful Insurance cons:

- Limited availability in non-Muslim countries

- Lack of standardization in some insurance markets

- Potentially higher costs than some basic conventional health insurance plans

- Takaful funds may not be enough during times of natural disaster or other periods with high claim volume

Conventional health insurance pros:

- Available across the world and in every insurance market

- Customizable and comprehensive healthcare benefits

- Some plans offer a global network of providers for those who travel abroad

Conventional health insurance cons:

- Not compliant with sharia for those who follow the religious law

- Insurance companies keep the profits made; does not act as investment

- Funds are not owned by individual policyholders

Choosing the Right Health Insurance Needs for You in Malaysia

Whether you want to purchase a takaful or conventional health insurance plan for your time in Malaysia, you should consider important factors like your religious beliefs, your budget, and your coverage needs.

- Consider Your Religious Beliefs: If you are Muslim and want to follow the sharia, you should choose takaful insurance for your healthcare coverage, as conventional health insurance is not compliant with the religious law.

- Consider Your Budget: Compare takaful plans and conventional health insurance plans and see which premiums and monthly payments fit your budget best. Pick the plan that you think will give you the best value for your money.

- Consider Your Coverage Needs: When choosing a health insurance plan, always choose the plan that you feel will adequately cover your desired healthcare needs. If you see yourself traveling outside of Malaysia frequently, consider an international health insurance plan.

For more information about health insurance plans for Malaysia, feel free to reach out to an experienced international insurance broker like Pacific Prime.

Frequently Asked Questions:

How are conventional and takaful insurance different from each other?

Conventional and takaful insurance are different in key ways, such as ownership of the funds. In takaful insurance, the participants in the takaful fund own the money available for claims, while in traditional health insurance, the insurance company owns the money available for claims.

Does takaful insurance offer good coverage?

Takaful insurance can have high-quality coverage, but this will depend on the provider you choose and the plan. Some takaful insurance plans may be more comprehensive than others.

What are the drawbacks of takaful insurance in Malaysia?

The drawbacks of takaful insurance are a lack of global coverage and standardization. Takaful is mainly available in Muslim countries and may not be available elsewhere. It lacks standardization as well due to its limited scope.

Is takaful insurance expensive?

Takaful insurance cost will depend on the specific benefits and coverage included in the policy and the chosen operator. Some insurance plans may be more expensive than others if they provide more benefits, and it has the potential to be more expensive than conventional health insurance.

Conclusion: Compare Plans and Quotes Now

Takaful insurance and conventional health insurance offer different advantages and disadvantages to expats in Malaysia. Taking your time comparing the two insurance options can help you make the best choice for your time abroad.

Are you interested in conventional health insurance plans? Pacific Prime is partnered with a wide variety of international health insurance providers, and can help you find the best fit for your needs.

As a global health insurance broker who specializes in expat health insurance, Pacific Prime can offer a wealth of professional expertise and services. Our tailor-made policies suit every budget and health care need for expats and travellers across the world.

Contact Pacific Prime to discuss, free of charge, a range of health insurance services available for you, your loved ones, or your group. To get a no-obligation, free price comparison quote, visit our website today!

If you’re interested in reading more articles for expats in Malaysia, check out our following blog posts:

Serena earned her Bachelor’s Degree in Psychology from the University of British Columbia, Canada. As such, she is an avid advocate of mental health and is fascinated by all things psychology (especially if it’s cognitive psychology!).

Her previous work experience includes teaching toddlers to read, writing for a travel/wellness online magazine, and then a business news blog. These combined experiences give her the skills and insights she needs to explain complex ideas in a succinct way. Being the daughter of an immigrant and a traveler herself, she is passionate about educating expats and digital nomads on travel and international health insurance.

- How to Compare Travel Insurance Plans the Smart Way – October 21, 2025

- Best Hospitals in the UAE: Top Picks in Dubai and Abu Dhabi – October 21, 2025

- How Much is a Doctor Visit in Dubai Without Insurance? – October 21, 2025